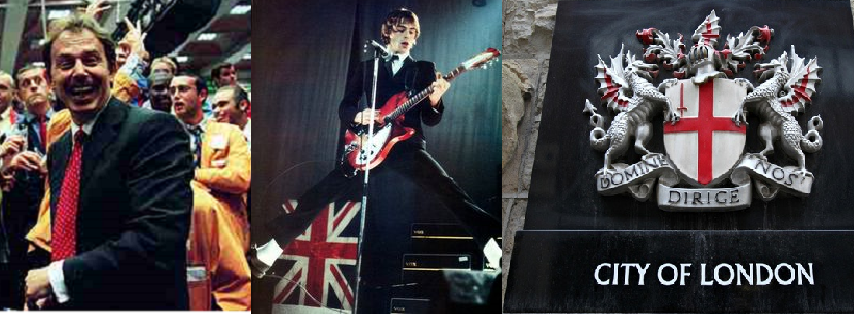

This is a tribute to the London Forex markets and currency trading in the wild good old days 1980's and 1990's where Essex boys once rocked the City.

Monday to Friday expletive after expletive, rough and ready London boys moving millions, Friday night curry and chips, smash ups, the Jam and Oasis, Tony Blair beaming with a newly found confidence and David Beckham half-way line wonder goals. Something's gone missing today as the computer takes over our world and the British currency culture rests in peace. Inspiration has truly died at the heart of the global economic time clock. The Essex boys have long since gone and the mod cons have brought us to a whole new dangerous era of artificial intelligence and computer trading programs.

As far back as the 1960's trading currencies was such a mundane sleepy affair. Overnight positions were simply not tolerated. The Old lady was averse to the culture of risk soon as Bretton woods collapsed and the oil crisis pushed us all to a global meltdown of the 70's. Central banks around the world monitored their balance of payments with iron rigidity as the Vietnam War plugged on and the Gold Standard fell apart only to be followed by the twin Opec shocks of 1973 and 1979. The international economy was in an alarming state of flux. Order was now disorder. Western governments no longer saw a rationale to adhere to the fixed currency system under the Bretton Woods Gold Standard agreement. Their central banks now with a mandate to pump up the credit. Thus came about the birth of the leveraged balance sheet and bottomless credit that led traders to run amok in the 00's, the noughties, with the easy credit culture of Alan Greenspan. A whole new world of currency bravado in a no rules arena was born. The Opec shocks in particular had woken up the financial system to deal with run away inflation in new ways in the currency markets and in fixed income open market operations. Truly the world would no  longer be a cozy arrangement for the genteel currency traders in bowler hats and ties. A new vibrant dynamism had arisen as a counter measure to the rapid problems of petrodollar inflation. Never had Great Britain felt the sheer raw nerve of energy since the 19th century when British merchant banks roamed the world financing deals. A new pulse of 20th century British banking had arrived with a new definition of mercantile aggression. But this time at its very core the shape of the banking heart had changed. At the very center of that dynamism there were the young men picked up from the streets to ply a new trade in the currency halls. The time of the Essex Boys had arrived. The spirit of youthful fisticuffs could now translate itself in a new unfettered arena. Deep within the epi-center something had to change to kick start the moribund complacency that nearly got the British stuck in the first place in the 1970's. On the threshold of the the London Currency Markets it was time for a change.

longer be a cozy arrangement for the genteel currency traders in bowler hats and ties. A new vibrant dynamism had arisen as a counter measure to the rapid problems of petrodollar inflation. Never had Great Britain felt the sheer raw nerve of energy since the 19th century when British merchant banks roamed the world financing deals. A new pulse of 20th century British banking had arrived with a new definition of mercantile aggression. But this time at its very core the shape of the banking heart had changed. At the very center of that dynamism there were the young men picked up from the streets to ply a new trade in the currency halls. The time of the Essex Boys had arrived. The spirit of youthful fisticuffs could now translate itself in a new unfettered arena. Deep within the epi-center something had to change to kick start the moribund complacency that nearly got the British stuck in the first place in the 1970's. On the threshold of the the London Currency Markets it was time for a change.

longer be a cozy arrangement for the genteel currency traders in bowler hats and ties. A new vibrant dynamism had arisen as a counter measure to the rapid problems of petrodollar inflation. Never had Great Britain felt the sheer raw nerve of energy since the 19th century when British merchant banks roamed the world financing deals. A new pulse of 20th century British banking had arrived with a new definition of mercantile aggression. But this time at its very core the shape of the banking heart had changed. At the very center of that dynamism there were the young men picked up from the streets to ply a new trade in the currency halls. The time of the Essex Boys had arrived. The spirit of youthful fisticuffs could now translate itself in a new unfettered arena. Deep within the epi-center something had to change to kick start the moribund complacency that nearly got the British stuck in the first place in the 1970's. On the threshold of the the London Currency Markets it was time for a change.

The late 1970's and early 1980's was an amazing Era of changes in the British banking world. Culturally, Britain was about to get a massive adrenalin shock as sweeping social changes would become the cry of the day. This was the new Big Bang resulting from a British identity crisis in the 1970's. Prior to the Big Bang which saw Britain emerge from it's identity crisis to carve out a new definition

of British banking, the London trading floors were replete with public schoolboys who sought to

make a steady career in a respectable manner.  Creed should dictate that

upon graduation the public schoolboy would enter the military, clergy,

law or banking. However, largely thanks to a new social revolution

finding its expression of commonality and spiritual bonding starting

with the Beatles in the 1960's and growing through the Rolling Stones in

the 1980's to the final release of absolute raw energy of expression

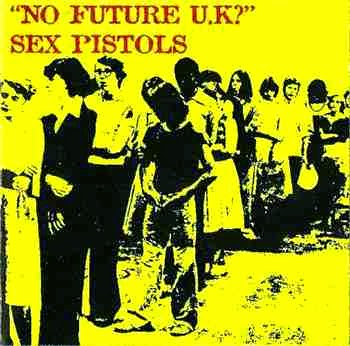

with the Sex Pistols in late 70's, society was beginning to transform

itself and the doors to the trading world were being torn asunder. But

The 1980's saw vast changes across British culture. From David Bowie to the Sex Pistols and

the Stranglers, song after song, lyrics would belt out the urgent cry

for change. No future they would belt out. Culture was in a state of

shock to change and find a better path forward. From the old the new shall always emerge. Only time would tell the truth as London sought to redefine itself in the modern world.

Creed should dictate that

upon graduation the public schoolboy would enter the military, clergy,

law or banking. However, largely thanks to a new social revolution

finding its expression of commonality and spiritual bonding starting

with the Beatles in the 1960's and growing through the Rolling Stones in

the 1980's to the final release of absolute raw energy of expression

with the Sex Pistols in late 70's, society was beginning to transform

itself and the doors to the trading world were being torn asunder. But

The 1980's saw vast changes across British culture. From David Bowie to the Sex Pistols and

the Stranglers, song after song, lyrics would belt out the urgent cry

for change. No future they would belt out. Culture was in a state of

shock to change and find a better path forward. From the old the new shall always emerge. Only time would tell the truth as London sought to redefine itself in the modern world.

Creed should dictate that

upon graduation the public schoolboy would enter the military, clergy,

law or banking. However, largely thanks to a new social revolution

finding its expression of commonality and spiritual bonding starting

with the Beatles in the 1960's and growing through the Rolling Stones in

the 1980's to the final release of absolute raw energy of expression

with the Sex Pistols in late 70's, society was beginning to transform

itself and the doors to the trading world were being torn asunder. But

The 1980's saw vast changes across British culture. From David Bowie to the Sex Pistols and

the Stranglers, song after song, lyrics would belt out the urgent cry

for change. No future they would belt out. Culture was in a state of

shock to change and find a better path forward. From the old the new shall always emerge. Only time would tell the truth as London sought to redefine itself in the modern world.

With a new sense of power and sense of urgency to accumulate

and dominate that new position the London banks and brokerages and

counting and discount houses turned to a new form of trader that would befit the role

of cutting -  edge adventurism reminiscent of the 19th century Victorian Era Empire building which saw English lads being flung across the far stretches

edge adventurism reminiscent of the 19th century Victorian Era Empire building which saw English lads being flung across the far stretches

edge adventurism reminiscent of the 19th century Victorian Era Empire building which saw English lads being flung across the far stretches

and waters for Queen and Country. A new

Great War was only just around the corner. After years of industrial decline

and economic malaise it took a new domineering woman to enthuse the

vision of London's financial dominance. Loved and loathed in equal

measure, Margaret Thatcher more than any British politician of the

century, inspired the great City of London to bask in its newly found

financial prowess with the liberation of the currency markets. Britain was an industrial nation in decline in the early 1980's. But the new Conservative Prime Minister saw a new future for Britain as banker to the world. The old Britain was ruthlessly dismantled as she crushed the Unions. To build a new house one must take apart the old, heartlessly. The London banking market, and in particular, the currency markets, had to find a new way forward. This system of old tie network was simply not working anymore in the 1980's. Meritocracy was the new creed. Prospects should not be based upon a school and a college. Britain had lost its post war dynamism with rapid social stagnation. The only way forwards was to apply a massive jolt. The Banks needed a new idea and new blood if Britain was to go forwards and define itself in the 1980's.

The City of London and it's hierarchical system off management could no longer look to the old guard for leadership and inspiration. Corporate leadership and visions in the City was dire. Such a culture clash of trading and management eventually came to the fore much later in the 1990's with the Barings bank debacle. 300 years of illustrious history down the tubes just like that. It was the old guard that had failed the venerable Barings bank in 1995 so miserably. by the 1990's the financial markets were already truly global. The flutter of the wings of a butterfly in Tokyo would ripple and cause havoc in London. Management simply could not comprehend the trades of one certain, now infamous, Nick Leeson. Thus the dear old bank,

I can remember living close to Piccadilly at Green Park in Mayfair at the time in the early 1990's and I could never sleep with that infernal racket of lorries carrying fruit cargo at 3am in the morning heading for the markets. London truly was a place that did not sleep. 5am every morning rain, sleet and snow I would scurry to the Green Park underground station to get the first train to take me to the square Mile at bank station. I have worked in both London and New York and there is quite a difference between the 2 great financial communities. In New York money was brash and open for everyone to see, but in London power was not quite visible; it was a quiet murmur of continuity. London could not sleep and turn itself off now. It took Margaret Thatcher to make us all realize that Britain was truly and rightly the center of the global clock and we need to make money from this strategic advantage. We had to shake things up and find our pulse again. An early morning stroll through the

fish meat and veg markets would soon confirm what many top bankers already knew; a vast recruit base of early morning traders that could

count faster than any computer of the time and with deft hand signals

could compete and cut a trade in fury to market bid in

live auction

process. A new Accidental Hero had been found readily available to join the troops at the front line. Financial jingoism and no holds barred would ensure that London had to grow at any cost. Margaret Thatcher had instilled a new enthusiasm to throw open the doors and embrace the world to transform a largely manufacturing nation into a service economy. Recruitment sans creed sans differentiation would be needed for a new phase of Empire building, the kind of global power play for financial dominance that would require a new swashbuckling bravado on all the City trading floors. Indeed for a tiny nation that had once spanned the globe, it only needed the spark to reignite an Anglo assertiveness and aggressiveness in the currency markets.

{kind=link}

No more soft comely David Cassidy look-alikes were welcome. Flares were out. Direct to the point was the new in thing. In the 1980's they came in droves, 18 years old, sometimes as young as 16 years even, straight out of high school and college, they would pack the London brokerages and provide a constant stream of aggressiveness that would  ensure that the City of London could compete and dominate in this new unregulated currency market. They came in their legions. They new how to be pushed and more importantly they new how to scrap and push back harder. All hours of the day they were up for it. Dollar Yen, No problems mate, all hours the day, hit the bid book the offer, bank the spread, Japanese banker on one phone, Swiss banker on the other, "Dollars to Japan, Yen to Frankfurt, : you're done 5 million" - then the next trade and the next and so on. Any time mate. All day long on the phone and watching the cheapest offers and the highest bids to lock party A to party B and book a fast trade in 20 seconds flat. They became popularly known as Essex boys; a fact derived from the proximity of the country of Essex close to the City of London. Young boys who had no other outlet for expression except the meat and veg markets, football and a passion for music were suddenly being called upon everywhere with recruitment to the banking industry. They had the stamina to launch London. Young, assertive, aggressive; they offered an instant channel and the City was totally bereft of that and it knew it. London needed young fresh blood and London had plenty of that in a tough assertive youth ready for the cut and the chase in the global financial markets. Essex Boys suddenly becoming men and sent off to a new financial war, some without even a first shave, to fight for Queen and country against the Almighty Dollar the Mark the Yen and everything else. Playground scrappers suddenly cutting their manhood shaving pips, hunting arbitrage, making instant spreads between bid and offers. Teenage flicks had arrived in the genteel City with a whole new vibrant energy. Counting their first paychecks in disbelief many the lads would habituate the City drinking halls which were suddenly becoming renown for a boisterous and younger crowd of trade. They could shout, they could count, but most importantly, they could think, under pressure, they could perform.

ensure that the City of London could compete and dominate in this new unregulated currency market. They came in their legions. They new how to be pushed and more importantly they new how to scrap and push back harder. All hours of the day they were up for it. Dollar Yen, No problems mate, all hours the day, hit the bid book the offer, bank the spread, Japanese banker on one phone, Swiss banker on the other, "Dollars to Japan, Yen to Frankfurt, : you're done 5 million" - then the next trade and the next and so on. Any time mate. All day long on the phone and watching the cheapest offers and the highest bids to lock party A to party B and book a fast trade in 20 seconds flat. They became popularly known as Essex boys; a fact derived from the proximity of the country of Essex close to the City of London. Young boys who had no other outlet for expression except the meat and veg markets, football and a passion for music were suddenly being called upon everywhere with recruitment to the banking industry. They had the stamina to launch London. Young, assertive, aggressive; they offered an instant channel and the City was totally bereft of that and it knew it. London needed young fresh blood and London had plenty of that in a tough assertive youth ready for the cut and the chase in the global financial markets. Essex Boys suddenly becoming men and sent off to a new financial war, some without even a first shave, to fight for Queen and country against the Almighty Dollar the Mark the Yen and everything else. Playground scrappers suddenly cutting their manhood shaving pips, hunting arbitrage, making instant spreads between bid and offers. Teenage flicks had arrived in the genteel City with a whole new vibrant energy. Counting their first paychecks in disbelief many the lads would habituate the City drinking halls which were suddenly becoming renown for a boisterous and younger crowd of trade. They could shout, they could count, but most importantly, they could think, under pressure, they could perform.

ensure that the City of London could compete and dominate in this new unregulated currency market. They came in their legions. They new how to be pushed and more importantly they new how to scrap and push back harder. All hours of the day they were up for it. Dollar Yen, No problems mate, all hours the day, hit the bid book the offer, bank the spread, Japanese banker on one phone, Swiss banker on the other, "Dollars to Japan, Yen to Frankfurt, : you're done 5 million" - then the next trade and the next and so on. Any time mate. All day long on the phone and watching the cheapest offers and the highest bids to lock party A to party B and book a fast trade in 20 seconds flat. They became popularly known as Essex boys; a fact derived from the proximity of the country of Essex close to the City of London. Young boys who had no other outlet for expression except the meat and veg markets, football and a passion for music were suddenly being called upon everywhere with recruitment to the banking industry. They had the stamina to launch London. Young, assertive, aggressive; they offered an instant channel and the City was totally bereft of that and it knew it. London needed young fresh blood and London had plenty of that in a tough assertive youth ready for the cut and the chase in the global financial markets. Essex Boys suddenly becoming men and sent off to a new financial war, some without even a first shave, to fight for Queen and country against the Almighty Dollar the Mark the Yen and everything else. Playground scrappers suddenly cutting their manhood shaving pips, hunting arbitrage, making instant spreads between bid and offers. Teenage flicks had arrived in the genteel City with a whole new vibrant energy. Counting their first paychecks in disbelief many the lads would habituate the City drinking halls which were suddenly becoming renown for a boisterous and younger crowd of trade. They could shout, they could count, but most importantly, they could think, under pressure, they could perform.

What is it about colorful jackets? in the 1980's and 1990's stockbrokers wore their grey suits and the futures guys were wearing all sorts of color jackets. But as for us, the heart and soul and backbone of the City, we were the shirt and tie nitty gritty boys getting our hands dirty, grinding 2 pip spreads minute after minute.In the early 1990's I can recall one day walking in the City down Cannon Street beside the old LIFFE buildings before it got taken over by Euronext. I was with 2 friends for a lunch break and there before us suddenly appeared this cock of the walk colorful peacock strutting about for a sandwich like God's own gift for mirrors. The first reaction of my friends was to stamp on his shoes. However I carefully reminded my colleagues that this cocky piece of art was handling more money in his fingers than the national debt Portugal! Young, brash, 22 years something, Essex born - knows his worth, knows his place, knows his time and knows you're not going to stand in his face. On the streets of London in the 1990's it wasn't altogether too crass to flaunt your value in a City that was full of young aspiring Essex boys. Either you were a Cockney ex-fruit trader or ex serviceman but whatever you were ex, you were now a financial futures trader. And that meant a lot in a new financial world that comes to respect the show of trophies, and I must say that LIFFE that time did have some very colorful jackets indeed.

Euronext. I was with 2 friends for a lunch break and there before us suddenly appeared this cock of the walk colorful peacock strutting about for a sandwich like God's own gift for mirrors. The first reaction of my friends was to stamp on his shoes. However I carefully reminded my colleagues that this cocky piece of art was handling more money in his fingers than the national debt Portugal! Young, brash, 22 years something, Essex born - knows his worth, knows his place, knows his time and knows you're not going to stand in his face. On the streets of London in the 1990's it wasn't altogether too crass to flaunt your value in a City that was full of young aspiring Essex boys. Either you were a Cockney ex-fruit trader or ex serviceman but whatever you were ex, you were now a financial futures trader. And that meant a lot in a new financial world that comes to respect the show of trophies, and I must say that LIFFE that time did have some very colorful jackets indeed.

Euronext. I was with 2 friends for a lunch break and there before us suddenly appeared this cock of the walk colorful peacock strutting about for a sandwich like God's own gift for mirrors. The first reaction of my friends was to stamp on his shoes. However I carefully reminded my colleagues that this cocky piece of art was handling more money in his fingers than the national debt Portugal! Young, brash, 22 years something, Essex born - knows his worth, knows his place, knows his time and knows you're not going to stand in his face. On the streets of London in the 1990's it wasn't altogether too crass to flaunt your value in a City that was full of young aspiring Essex boys. Either you were a Cockney ex-fruit trader or ex serviceman but whatever you were ex, you were now a financial futures trader. And that meant a lot in a new financial world that comes to respect the show of trophies, and I must say that LIFFE that time did have some very colorful jackets indeed.

Black Wednesday left us all with an indelible and colorful memory. Nobody had a clue who George Soros was but we all certainly loved him or loathed him by the end of this day. Certainly Norman Lamont wouldn't forget him; the interest rate debacle had cost him his political career eventually. But it did raise an important issue about central banks and their real ability to defend a national currency when large speculators are working the markets against them. I recall somewhere in the mid 1990's I was rushing out of the Grosvenor Hotel, from the back entrance on Park Street, just behind leafy Park Lane, and as I came out after a few drinks with some friends, lo and behold, the graceful man himself trundling up in a smart grey coat. I heard he had just taken up some lucrative consultancy. So I couldn't help myself but asking him rather cheekily if he remembered Mr Soros. Needless to say Mr Lamont was not amused as I simply grinned and walked away! I did feel sorry for him though as his exit from politics after the crisis was nothing short of dignified. and most of us hated George Soros but that was life; the markets are mean and full of nasty vultures.  What was the final bill? Of course it was nothing to do with poor Mr Lamont; he was a great Minister and widely respected and we all felt sorry for him hiking rates to defend the Pound. But the whole effort was gallantly futile like the charge of the Light Brigades. Eventually the decision to defend Sterling by hiking interest rates may have cost the Exchequer some 30 Billion Sterling. Quite literally we were throwing baked beans at a charging rhinoceros. It was the global market that determined the value of Sterling and we could not fight the trigger that Mr Soros sparked that day. But in the long run, if this was the worst that could have ever happened to London, then the City retained some greatness in its awe inspiring resilience and its determination to fight back to bring stability to the currency markets. John Major and Norman Lamont were pilloried beyond dignity in the press. But they had the graciousness to guide the London financial markets through choppy seas. It is often in times of crisis we find our true best. Although this day, the 16th September 1992 would ever be recalled with infamy, the crash of sterling thru it's set ERM parity vs the Deutsche Mark, saw the resilience of London currency traders as they would fight pip by pip against the flood of sell orders. What strikes me the most on that fateful day was the absolute stoicism with which the London currency traders acted in the face of a flip-flop political mess of UK interest rate policy. They fought like tigers. Expletive after expletive there was simply no time when the cuffs were out. With hardy hearts no matter where Sterling lie,

What was the final bill? Of course it was nothing to do with poor Mr Lamont; he was a great Minister and widely respected and we all felt sorry for him hiking rates to defend the Pound. But the whole effort was gallantly futile like the charge of the Light Brigades. Eventually the decision to defend Sterling by hiking interest rates may have cost the Exchequer some 30 Billion Sterling. Quite literally we were throwing baked beans at a charging rhinoceros. It was the global market that determined the value of Sterling and we could not fight the trigger that Mr Soros sparked that day. But in the long run, if this was the worst that could have ever happened to London, then the City retained some greatness in its awe inspiring resilience and its determination to fight back to bring stability to the currency markets. John Major and Norman Lamont were pilloried beyond dignity in the press. But they had the graciousness to guide the London financial markets through choppy seas. It is often in times of crisis we find our true best. Although this day, the 16th September 1992 would ever be recalled with infamy, the crash of sterling thru it's set ERM parity vs the Deutsche Mark, saw the resilience of London currency traders as they would fight pip by pip against the flood of sell orders. What strikes me the most on that fateful day was the absolute stoicism with which the London currency traders acted in the face of a flip-flop political mess of UK interest rate policy. They fought like tigers. Expletive after expletive there was simply no time when the cuffs were out. With hardy hearts no matter where Sterling lie,  no matter the depths of political upheaval surrounding sterling, even the chaos of interest rate indecision by the Exchequer and the Bank of England, did not deter the City of London from fighting back inch by inch, pip by pip. London has a culture of aggressiveness that cannot be found in New York. With resilience London soon found itself stabilizing and expanding its dominating influence on the currency market global arena. London could take a smack in the mouth and still stand tall. To the credit of the trading room dealers George Soros maybe have taken a few Bob's worth, but would ever become unable to repeat that kind of feat in London again. The rapid decline and reset of Sterling was more to do with political turmoil than the smooth working mechanism of making trades to satisfy the global community and it's currency needs. Politics moves a currency but economic reality restores it's true value. Large speculators can thrive on panic and media disinformation but reality will always reset. There is a distinctly silent murmur about London, a quiet knowing hum that speaks of real power behind every grey stone wall in the city. Not like New York where everything has to be lit up with glamor for all to see.

no matter the depths of political upheaval surrounding sterling, even the chaos of interest rate indecision by the Exchequer and the Bank of England, did not deter the City of London from fighting back inch by inch, pip by pip. London has a culture of aggressiveness that cannot be found in New York. With resilience London soon found itself stabilizing and expanding its dominating influence on the currency market global arena. London could take a smack in the mouth and still stand tall. To the credit of the trading room dealers George Soros maybe have taken a few Bob's worth, but would ever become unable to repeat that kind of feat in London again. The rapid decline and reset of Sterling was more to do with political turmoil than the smooth working mechanism of making trades to satisfy the global community and it's currency needs. Politics moves a currency but economic reality restores it's true value. Large speculators can thrive on panic and media disinformation but reality will always reset. There is a distinctly silent murmur about London, a quiet knowing hum that speaks of real power behind every grey stone wall in the city. Not like New York where everything has to be lit up with glamor for all to see.

What was the final bill? Of course it was nothing to do with poor Mr Lamont; he was a great Minister and widely respected and we all felt sorry for him hiking rates to defend the Pound. But the whole effort was gallantly futile like the charge of the Light Brigades. Eventually the decision to defend Sterling by hiking interest rates may have cost the Exchequer some 30 Billion Sterling. Quite literally we were throwing baked beans at a charging rhinoceros. It was the global market that determined the value of Sterling and we could not fight the trigger that Mr Soros sparked that day. But in the long run, if this was the worst that could have ever happened to London, then the City retained some greatness in its awe inspiring resilience and its determination to fight back to bring stability to the currency markets. John Major and Norman Lamont were pilloried beyond dignity in the press. But they had the graciousness to guide the London financial markets through choppy seas. It is often in times of crisis we find our true best. Although this day, the 16th September 1992 would ever be recalled with infamy, the crash of sterling thru it's set ERM parity vs the Deutsche Mark, saw the resilience of London currency traders as they would fight pip by pip against the flood of sell orders. What strikes me the most on that fateful day was the absolute stoicism with which the London currency traders acted in the face of a flip-flop political mess of UK interest rate policy. They fought like tigers. Expletive after expletive there was simply no time when the cuffs were out. With hardy hearts no matter where Sterling lie, no matter the depths of political upheaval surrounding sterling, even the chaos of interest rate indecision by the Exchequer and the Bank of England, did not deter the City of London from fighting back inch by inch, pip by pip. London has a culture of aggressiveness that cannot be found in New York. With resilience London soon found itself stabilizing and expanding its dominating influence on the currency market global arena. London could take a smack in the mouth and still stand tall. To the credit of the trading room dealers George Soros maybe have taken a few Bob's worth, but would ever become unable to repeat that kind of feat in London again. The rapid decline and reset of Sterling was more to do with political turmoil than the smooth working mechanism of making trades to satisfy the global community and it's currency needs. Politics moves a currency but economic reality restores it's true value. Large speculators can thrive on panic and media disinformation but reality will always reset. There is a distinctly silent murmur about London, a quiet knowing hum that speaks of real power behind every grey stone wall in the city. Not like New York where everything has to be lit up with glamor for all to see.

When China wants to buy copper and soybeans from the

Americas transactions are carried out in London. When Apple Inc. and Exxon want

to sell products across a global platform, payments are received in kind in

London. So large are the Euro Dollar deposits in fact that they became a huge

source of finance for the blossoming credit derivatives market during the

credit boom up to 2008. Many CDO and CMO credit derivatives were packaged in

London due to its vast resources of currency deposits. American and Japanese and now Chinese companies will always hold vast accounts of currencies in London for settlement between the time zones. Moreover that money cannot just sit there and burn a gigantic hole in the banks. it gets lent out in the interbank market for short periods of time from 1 to 90 days with huge liquidity and as far ahead as up to 1 year as banks take advantage of huge currency deposits to lend to each other through swaps and other derivatives. According to the Bank for International Settlements the derivatives market for the Euro currency alone is estimated to be 26 trillion dollars in 2015 alone. The spot for forward 90 day had now grown into a massive creature of risk and asset allocation. As computing power exponentially grew to serve so too did the need for financial engineering grow and London maintained it's position at the front of the forex markets as the need for derivatives in London grew.

So finally by the late 1990's the world of the Essex boys would come to an end with the arrival of the 00's, otherwise known as the noughties. Changes are eternal. Changes are inevitable. As the Essex Boys replaced the public and grammar school traders with banks in search of new dynamism, soon the trading world would become enamored with a new archetypal figure - The Quant. But it was way back in the mid 1990's when I first felt that distant horizon tremor of another era of sweeping changes. That was the year I suddenly knew that the whole world of currency trading was about to change yet again as the world of derivatives trading started to grow exponentially. Technology improves. Only the other day we used to sport those huge electronic 3 function watches with gust and bravado! so change was always going to be inevitable. One day when we were told to stay behind after market close for a brief one hour lecture, we were introduced to a whole brave new world called - the Internet. The older traders would fidget and scratch their heads. The younger traders would listen keenly. Up to that date most of the London trading floors were still a bunch of old Reuters dealer systems piled up on top of each other with a million phone wires running across everywhere along walls and along the floors. Although Windows PC's were being gradually introduced with the new vogue of office automation, still in large the London dealer system was phone-based with the assistance of our old Reuters Monitor Dealing Service monitors. Not only that; the floors in those days were so noisy one would always have to go home with a hoarse voice because electronic trading hadn't yet been introduced. But within a year electronic trading had commenced and the older traders were being flung out redundant. The machine had finally arrived. But it took the technicians nearly 3 years to pull put all the wires from the old machines because quite honestly none of the software engineers had a clue how many different software systems were being used and were quite scared to pull the plug in case the whole trading floor ground to a halt. the software men had to virtually rebuild an entire new trading network from scratch before they could close the old trading system. I can still remember how many laughs we had at the technicians just staring in to space and wondering which wire goes where! But those laughs are now forgotten and the noise of a London trading room but a ghostly echo. The time had come for the new number crunching Quant who could manipulate electronic trading with vast data input.

That was an era now long gone for even in it's midst Time Magazine had already forewarned the dark and abject Orwellian shape of things to come. A bright new plastic and metal Mod Con. In 1982 Time Magazine did not select any human for it's prestigious annual accolade of "Man Of The Year." Instead, it chose the computer.... Today, the currency trading arena is indeed a frightening world of uncertainty as the computer program comes to play an increasing role in the business community today. The whole world is changing so fast it has even been mooted that industries like the credit card plastic in  our wallets and our express deliveries via Fedex and DHL, may become a thing of the past within the next 10 years as mobile computing applications grow and distinctions between hardware devices become blurred. The recent chaos in the forex markets on January 16th when the SNB announced its decision to decouple from the Euro currency is a good example of this new world of currency trading. The announcement sent such a force of pressure to sell the EUR/USD that many large traders caught unawares were totally engulfed in a tsunami of selling. Most of the sales pressure came from secretive automated trading systems that many banks use and the result was a massive snowball through a whole line of sell stops that compounded into the day's rout. The computer program is estimated to have taken over near 50% of large bank trading activity in the currency markets today. Furthermore what really scares us the most is that the ultimate fail-safe has been removed - the element of human decision making; the gut feeling of a trader to go short, long or wait. When a currency quickly moves today, computer programs take decisions to buy or sell based upon complex parameters and back-tested data. Whether this is good or bad; it's simply too late to debate that question. Algorithm is here to stay; the new question now rises: how do we contain a new risk that a computer may accidentally move a market in a logical direction that may not be the best direction after all. Isaac Asimov's 3 laws of robotics could easily be applied to a bank computer program that is built with a survival safety valve that would ensure the survival of the institution. But for the human mind, computer and robotic logic does not apply. a bank computer trading program based upon some immutable law of preservation does not necessarily result in the right course of action. otherwise Citibank and Deutsche Bank would have not lost money on January 16th. History has been defined by the many accidents of humanity. Where the currency markets are heading is a whole new world of logical assumption.

our wallets and our express deliveries via Fedex and DHL, may become a thing of the past within the next 10 years as mobile computing applications grow and distinctions between hardware devices become blurred. The recent chaos in the forex markets on January 16th when the SNB announced its decision to decouple from the Euro currency is a good example of this new world of currency trading. The announcement sent such a force of pressure to sell the EUR/USD that many large traders caught unawares were totally engulfed in a tsunami of selling. Most of the sales pressure came from secretive automated trading systems that many banks use and the result was a massive snowball through a whole line of sell stops that compounded into the day's rout. The computer program is estimated to have taken over near 50% of large bank trading activity in the currency markets today. Furthermore what really scares us the most is that the ultimate fail-safe has been removed - the element of human decision making; the gut feeling of a trader to go short, long or wait. When a currency quickly moves today, computer programs take decisions to buy or sell based upon complex parameters and back-tested data. Whether this is good or bad; it's simply too late to debate that question. Algorithm is here to stay; the new question now rises: how do we contain a new risk that a computer may accidentally move a market in a logical direction that may not be the best direction after all. Isaac Asimov's 3 laws of robotics could easily be applied to a bank computer program that is built with a survival safety valve that would ensure the survival of the institution. But for the human mind, computer and robotic logic does not apply. a bank computer trading program based upon some immutable law of preservation does not necessarily result in the right course of action. otherwise Citibank and Deutsche Bank would have not lost money on January 16th. History has been defined by the many accidents of humanity. Where the currency markets are heading is a whole new world of logical assumption.

our wallets and our express deliveries via Fedex and DHL, may become a thing of the past within the next 10 years as mobile computing applications grow and distinctions between hardware devices become blurred. The recent chaos in the forex markets on January 16th when the SNB announced its decision to decouple from the Euro currency is a good example of this new world of currency trading. The announcement sent such a force of pressure to sell the EUR/USD that many large traders caught unawares were totally engulfed in a tsunami of selling. Most of the sales pressure came from secretive automated trading systems that many banks use and the result was a massive snowball through a whole line of sell stops that compounded into the day's rout. The computer program is estimated to have taken over near 50% of large bank trading activity in the currency markets today. Furthermore what really scares us the most is that the ultimate fail-safe has been removed - the element of human decision making; the gut feeling of a trader to go short, long or wait. When a currency quickly moves today, computer programs take decisions to buy or sell based upon complex parameters and back-tested data. Whether this is good or bad; it's simply too late to debate that question. Algorithm is here to stay; the new question now rises: how do we contain a new risk that a computer may accidentally move a market in a logical direction that may not be the best direction after all. Isaac Asimov's 3 laws of robotics could easily be applied to a bank computer program that is built with a survival safety valve that would ensure the survival of the institution. But for the human mind, computer and robotic logic does not apply. a bank computer trading program based upon some immutable law of preservation does not necessarily result in the right course of action. otherwise Citibank and Deutsche Bank would have not lost money on January 16th. History has been defined by the many accidents of humanity. Where the currency markets are heading is a whole new world of logical assumption.

So here we are today where an age of assertive brashness has come to a grinding halt with the advent of the machine. Recently, in our beloved world of football, from the British club Tottenham Hotspur, Argentine manager Mauricio Pochettino was asked why he would keep expensive foreign signings on the bench in preference for local home-grown players Ryan Mason and Nabil Bentaleb. His answer simply boiled down to a recognition of distinct native aggression. The British have an innate stamina for the long haul fight for success. Unlike in European football the British fight right up to the maddening end. As French Tottenham player Benjamin Stambouli comically remarked, in France you would never see players run at each other in full attack right up until the last gasp and the final whistle. But The British just keep on going on like mighty dynamos. that would just about sum up the spirit of the 1980's and 1990's. Yet still even today, even after the US credit crisis of 2008, the liquidity problems of several UK banks and the quagmire of Euro debt today, the London financial markets today remain fiercely competitive, computer or no computer, London traders will push you back if you start standing in their face. Because unlike computer programs traders are not logical and that difference of opinion is what makes markets in the wonderful world of choice and opportunity.

In memory of long ago friday night pints, scuffles and midnight fish n chipees and early morning bus rides home, David Beckham wonder goals and scalping 3 pip spreads. Cheers all! and Good Luck For Tottenham Hotspur today in the Capital One Cup Final!

Pieter Bergli - DeLoren Trust Holdings

Currency markets education

Disclaimer - U.S. Government Required Disclaimer - Commodity Futures Trading Commission

Futures and Options trading involves risks of losses. No representation is being made that any reader and account will or is likely to achieve profits or losses similar to those that are being discussed on this blog http://forexeducationperspective.blogspot.com/. The past performance of any trading system or methodology discussed is not necessarily indicative of future results.

CFTC RULE 4.41 - HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.

All trades, patterns, charts, systems, etc., discussed in this blog http://forexeducationperspective.blogspot.com/ are for educative and illustrative purposes only and not to be construed as specific advisory recommendations for actual trades. Disclaimer - http://forexeducationperspective.blogspot.com/